fjrigjwwe9r3SDArtiMast:ArtiCont

class=>

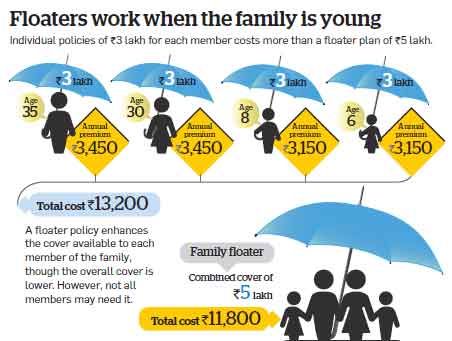

Rakesh Somani, 34, is looking for a health cover for his family, including his wife Ruchita, 30, and sons Rudraksh, 8, and Raghav, 2. Individual covers of Rs 3 lakh each will cost him Rs 13,200 a year. A floater cover of Rs 5 lakh will cost him Rs 11,800 a year. One of the biggest dilemmas faced by health insurance buyers is whether they should go for individual policies or a floating cover for the entire family. In an individual policy, the cost of the cover is generally lower compared with a floating plan.However, in the case of the latter, a higher cover is available to all members of the family since each member can avail of the combined cover. The logic is simple. There is a low probability that more than one or two family members will require hospitalisation in a year. It is a calculated risk which reduces the cost of the cover substantially.

| Floaters work best in case of young families. The premium is low because it is linked to the age of the eldest member in the plan. "A family floater cover is advisable when the oldest member is less than 45 years old," says Neeraj Basur, chief financial officer, Max Bupa Health Insurance.For 34-year-old Rakesh Somani, it is an ideal choice for insuring his family (see picture). "Since we are a young family and our healthcare costs are not too high, a floater plan of Rs 5 lakh should be sufficient for us," he says. Costly for older families However, the same may not be true for an older family, where the eldest member is more than 45 years old and the children are grown up. In such a case, individual policies may work out to be cheaper. The same is true if you want to insure an elderly member of the family. The premium can be prohibitive when you include a senior citizen (above 60) in the floater plan.

For instance, a Rs 3 lakh floater cover for a family of four, where the eldest member is 35 years old, will cost less than Rs 9,000 a year. However, if you add senior citizen parents (65 and 60 years), the premium jumps to Rs 52,500. "When older family members have to be covered, it is better to buy separate plans for them," says Gaurav D Garg, managing director & CEO, Tata AIG General Insurance.

Individual covers of Rs 3 lakh each for the two senior citizens would cost about Rs 30,000 (Rs 18,000 for the 65-year-old man and Rs 12,000 for the 60-year-old woman). This still works out cheaper than a combined floater for the entire six-member family.

|

|

Go for individual cover after 45

Taking an individual plan could also be an option when the eldest member of the family crosses 45 years. He can take a standalone policy for himself, while the rest of the family is covered under a floater plan. Insurers allow members to branch out and take individual policies when the plan comes up for renewal. This is also useful when a dependent child grows up and starts earning. He may need to buy a separate health insurance plan for his own family. Check if your insurer will carry forward the benefits accumulated by the individual in the floater plan when he shifts to the individual cover. This is important since there is a 3-4 month cooling off period for all claims as well as a 2-3 year waiting period before pre-existing diseases are covered by health insurance companies.

Top-up plans are cheaper

The health insurance provided by employers usually includes floater plans that cover the employee and his dependants. It is not advisable to depend entirely on such a cover because if you change jobs or stop working, your family may be rendered uninsured. If you think buying a fresh insurance plan is very expensive, go for a top up health cover. Top-up policies cover medical expenses beyond a certain threshold. Suppose an individual has an insurance cover of Rs 3 lakh from his employer and takes an additional top-up cover of Rs 5 lakh, with a deductible of Rs 3 lakh. If he is hospitalised for an illness and the bill comes to Rs 7 lakh, his employer’s cover will pay for the initial Rs 3 lakh and his top-up policy will pay the remaining Rs 4 lakh.

| The deductible in the top-up covers brings down their cost substantially. Since almost 85-90% of the claims are below Rs 3 lakh, the risk for insurance companies is minimal. Therefore, a top-up plan is 40-60% cheaper compared with a full-fledged cover. If a regular cover of Rs 3 lakh costs Rs 3,500, a top-up cover of Rs 5 lakh with a Rs 3 lakh deductible will cost only Rs 1,600. |

|

Industry News

Industry News