Latest articles on Life Insurance, Non-life Insurance, Mutual Funds, Bonds, Small Saving Schemes and Personal Finance to help you make well-informed money decisions.

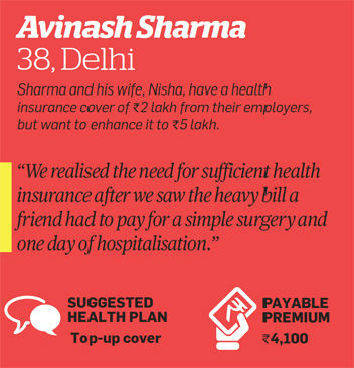

It takes an agent several days, even weeks, to convince a customer to buy health insurance. Yet, 10 minutes at the billing counter of a hospital were enough to persuade Avinash Sharma.

When the Delhi-based professional visited a friend, who had undergone a minor surgery in a private hospital last month, he was shocked to see the bill at the time of discharge. "A simple operation and one night’s hospitalisation cost him Rs 1.4 lakh. The cover from his employer covered only Rs 50,000 of the cost," he says. We are not surprised. Healthcare costs are rising at a fast clip. According to a survey by insurance consultancy firm, Towers Watson India, healthcare costs in India increased by 13.25% in 2011.

Case of Avinash Sharma

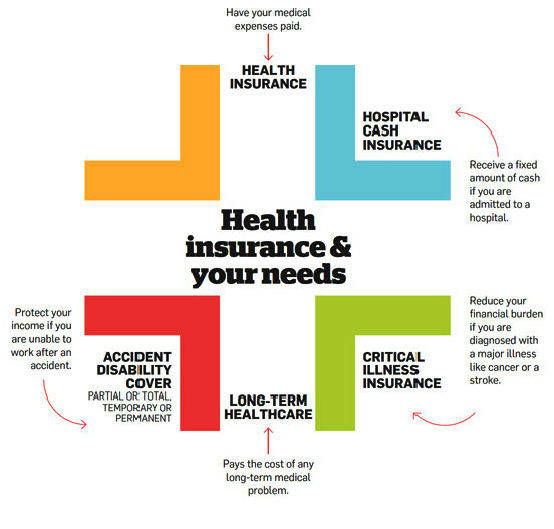

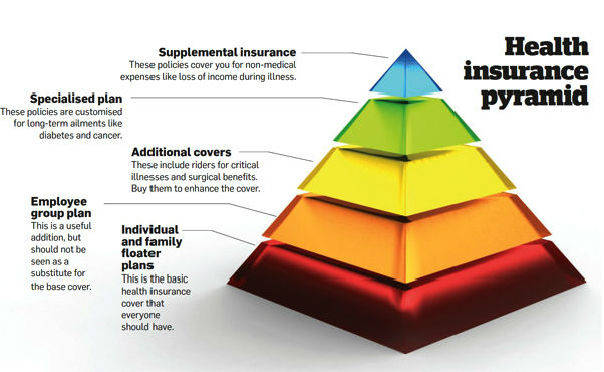

The rate of increase in 2012 is estimated to be roughly at the same level. The culprits: introduction of new medical technologies, over-prescription by doctors, and a general rise in medicine costs. Says Antony Jacob, CEO of Apollo Munich Health Insurance: "The treatment protocol for angioplasty today is vastly different from that followed five years ago. Many of these advanced medical technologies and procedures cost more." Sharma is now looking for a health insurance policy for his family. However, the vast array of choices before him is confusing. There are individual policies and family floater plans, policies that restore the limit after the claim and plans that cover critical illnesses or offer cash benefits on hospitalisation. How does one pick a suitable plan from this clutter? The answer is that your needs should define the type of policy you buy. Each type of health insurance policy fulfils a certain need (see graphic). The choice depends on the buyer’s age, family size and structure, and existing insurance cover.

|

|

|

| Living with dependent parents The family floater plan is not a good option if you want a cover for an older relative as well. This is because the premium rates in these plans are determined by the age of the oldest member. If you live with aged parents, it is advisable to go for individual policies rather than a family floater. Buy individual plans for them so that the premium for the rest of the family does not shoot up. Also, there is a greater likelihood of making a claim for an older person. So the floater plan will miss out on the no-claim bonus it might have otherwise received. |

|

Copyright © 2026 Design and developed by Fintso. All Rights Reserved

Industry News

Industry News